|

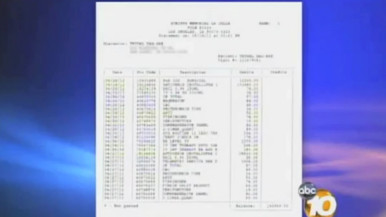

| Norwegian man Dag-Are Trydal was charged more than $100,000 for treatment for a rattlesnake bite. When HLN’s Robin Meade heard about it she said, "My jaw was dropping down. Yeah. Yeah, this is way too much. Excuse me, I would like a refund." People in Norway were shocked, as treatment in Norway would have been on the house. Some commenters in the Local called it typical hospital fraud in the U.S. |

Thursday, May 31, 2012

Norwegian man charged $100,000 for treatment of a snake bite in U.S.

Saturday, March 24, 2012

Supreme Court to take on Affordable Healthcare

THURSDAY, March 22 (HealthDay News) -- The most ambitious government health-care initiative since the Medicare and Medicaid programs of the 1960s, and the legislative landmark of President Barack Obama's presidency, is about to face its biggest challenge.

Starting Monday, the U.S. Supreme Court will hear an unprecedented six hours of arguments over three days on the constitutionality of the controversial and massive health-reform initiative known as the Affordable Care Act.

The law -- the first national legislative effort to rein in health-care costs -- aims to extend insurance coverage to more than 30 million Americans through an expansion of Medicaid and a provision that people buy health insurance starting in 2014 or face a penalty.

"There are 50 million people in this country who don't have health insurance. The Affordable Care Act will probably extend coverage to an estimated 30 to 32 million of those people," said Renee Landers, a professor at Suffolk University Law School in Boston.

The key sticking point in the legal showdown is whether Congress exceeded its authority with the law's so-called "individual mandate," which requires almost all adult Americans to maintain health insurance or risk a penalty in the form of a tax.

The individual mandate -- scheduled to take effect in January 2014 -- is the pivotal piece of the law.

"The requirement that people purchase insurance is the key to having health insurance be there for everyone when they need it," said John Rother, president of the National Coalition on Health Care, which works to achieve reform of the U.S. health-care system.

Opponents call the mandate a stunning government intrusion into the private lives of Americans and argue that Congress has no right to tell an individual to buy a certain product.

Grace-Marie Turner, president of the Galen Institute, a conservative public policy group, and a critic of the new law, is thrilled that the High Court has agreed to hear challenges to the legislation.

"This case is before the Supreme Court in record time. Two years from the law being enacted to the case being heard is really remarkable," Turner said. "And you have 26 states -- the majority of states -- challenging the law."

The Supreme Court will also hear arguments on whether the law is unconstitutional in requiring states to either comply with an expansion of Medicaid to cover more lower-income people without health insurance, or lose federal matching funding. At issue is the concept of "federalism," the division of powers between the federal and state governments.

Finally, the court will address "severability" -- that is, whether the individual mandate can be struck down while leaving the rest of the law intact.

In a recent New England Journal of Medicine commentary, Landers described arguments for and against severability.

Opponents have said that provisions of the legislation are too intertwined for the law to stand without the individual mandate. The Obama administration has said the law can still work without the mandate, but provisions such as prohibiting insurance companies from denying coverage to people with preexisting conditions would be greatly compromised without the mandate.

Budget office sees savings; opponents skeptical

Here's how the health-reform law is designed to provide health insurance to uninsured Americans:

- Individual mandate. It requires most adults to purchase health insurance or pay a tax penalty. By 2016, the phased-in penalty will reach either $695 or 2.5 percent of yearly taxable income, whichever is greater. People with incomes below tax-filing thresholds will be exempt from the provision. Up to 16 million people are projected to join the rolls of the insured under the mandate.

- Medicaid expansion. This would increase eligibility to all people under age 65 with annual incomes up to 133 percent of the federal poverty level -- about $14,850 for a single adult and $30,650 for a family of four in 2012. Non-disabled adults under 65 without dependent children were previously ineligible. Another 16 million people are estimated to gain insurance under the expansion.

- State-run insurance exchanges. They will be created to help small businesses and individuals purchase insurance through a more organized and competitive market.

In February 2011, the Congressional Budget Office estimated that savings from the Affordable Care Act would cut the federal deficit by $210 billion during the next decade.

But opponents say that the cost-cutting provisions probably won't work.

Devon Herrick, a health economist at the free-market National Center for Policy Analysis, said the law sets up a "slippery slope" that will increase costs, not lower them.

"If Congress and company have the legal authority to decide the minimum coverage you must have, all manner of lobbyists and special interests and providers for specific diseases will descend on Washington and state capitals, as they always have, to make sure that their respective services are covered by that mandate," Herrick said.

The law's supporters argue that without the requirement that people have insurance coverage while they're healthy, there won't be enough money in the risk pool to pay to take care of them when the need for health care eventually -- and inevitably -- arises.

"If people don't feel like paying, then get sick and go to the emergency room or the hospital, those people's costs will be added on to our insurance bills as they are today, which makes it much more expensive," Rother said.

Lower courts, different interpretations

The legal trail of challenges leading up to the Supreme Court has involved more than two dozen lawsuits and appeals.

Last June, the Cincinnati-based 6th Circuit Court of Appeals ruled that the individual mandate was valid because of the Constitution's Commerce Clause, which allows Congress to regulate commerce that takes place among states.

In August, a district judge in Florida ruled that the individual mandate was unconstitutional. However, the 11th Circuit Court of Appeals, which reviewed his decision, rejected that argument and found that the Affordable Care Act could stand even if the individual mandate provision were removed, Landers said.

Then in November, the U.S. Court of Appeals for the District of Columbia also upheld the individual mandate based on the Commerce Clause.

The U.S. Supreme Court chose to review the Florida case, which now includes 25 other states as plaintiffs, along with the National Federation of Independent Business.

The law has been controversial since it was passed by Congress and signed by Obama in March 2010. Poll after poll has found that Americans don't like the individual mandate. But a recent Harris Interactive/HealthDay poll revealed that people are starting to warm up to certain key provisions of the law -- such as the ban on insurance companies turning away applicants with preexisting health problems.

Some popular provisions -- including allowing children to stay on their parents' health plans until age 26 -- are already in place.

Other provisions meant to help older Americans began in 2011, with changes to continue through 2020.

Medicaid expansion a vital component of the law

States must comply with the Medicaid expansion no later than 2014. But some worry that a big influx of new enrollees could strain medical specialties such as obstetrics/gynecology, pediatrics and family practice.

Dr. Peter Carmel, president of the American Medical Association, called the expansion "an important step in the right direction," even though many "physicians are currently unable to accept Medicaid patients due to low reimbursement rates."

Added Dr. Glen Stream, president of the American Academy of Family Physicians: "For the time being, [the new law] seems like the best option to get everyone covered with health insurance. Otherwise, people are carved out from good primary-care services, good preventive care and wellness services, and care of their chronic illnesses until sometimes it's too late."

The Supreme Court ruling is expected in June. The court could go one of several ways:

- It could rule the individual mandate is unconstitutional and the entire law invalid.

- It could rule the mandate is constitutional and the entire law can stand.

- It could reach a middle ground: that the individual mandate is unconstitutional but the rest of the law can stand.

- It could decline to rule on the case and the health reforms would proceed.

The decision may pivot on the vote of Justice Antonin Scalia, a court conservative. Suffolk University's Landers said that in a previous case that centered on the Commerce Clause, "Scalia wrote a concurrence in which he took a very broad view of Congress' authority. So I think he has a lot of work to do to get himself out from under that concurrence."

She said it's also possible -- though unlikely -- that the court could decide to delay ruling on the case altogether.

That would be a major setback for opponents, said Turner at the Galen Institute. "By 2017, 'Obamacare' would have such deep roots that it would be hard to overturn," she said.

Whatever the court decides, it will provide plenty of fodder for the 2012 elections. And even if the Affordable Care Act survives the legal challenge, Landers said, "with upcoming elections -- a new Congress -- it doesn't mean that everything is set for all time."

Sunday, September 18, 2011

Young People today will have to save a lot more than their parents did for retirement

Twentysomethings will need to save much more than their parents did for retirement

Retirement won't be impossible for Generations X and Y, but they will need to save considerably more than the baby boomers to make up for less employer and government help. Fewer young people have access to generous retirement benefits, including traditional pensions and retiree health insurance. And anyone born in 1960 or later must wait an extra year, until age 67, to claim the full amount of Social Security they are entitled to. Those who claim at the same age their parents did will get less. Here are some ways 20- and 30-somethings can get on track to retire comfortably.

Set a worthy goal. In a 2010 survey of 226 registered investment advisors commissioned by Scottrade Advisor Services, more than three-quarters (77 percent) suggested a retirement savings goal of at least $2 million for members of Generation Y, defined by the study to include those ages 18 to 26. Sixty-eight percent of the investment advisers said members of Generation X should also aim to save more than $2 million. "For a generation Y person who thinks she wants to retire at around age 70 who is going to have slightly above-average annual expenses, $2 million is probably the right number," says Michael Farr, president of the Washington, D.C., investment firm Farr, Miller, & Washington and author of A Million Is Not Enough: How to Retire With the Money You'll Need. But he cautions, "Most people who have high incomes and the ability to set aside $2 million will likely have more expensive lifestyles."

However, other studies have found that young people may be able to get by on less in retirement. Human resources consulting firm Aon Hewitt calculated that Generation Y workers, who it defines as people ages 18 to 30, will need 18.7 times their final pay for retirement, including Social Security, traditional pension plans, and personal savings, to maintain their current standard of living after retirement at age 65. For someone whose final salary is $75,000, that's just over $1.4 million, and Social Security will provide part of that. For Generation Xers ages 31 to 45, Aon Hewitt estimates they will need 16.1 times their final salary to pay for retirement. "A higher earner will probably continue to spend more in retirement," says Janet Tyler Johnson, a certified financial planner and president of JATAJ Wealth Management in Fitchburg, Wis. "It's really dependent on how much you need in retirement."

Take advantage of employer help. Getting to $2 million will take some effort, even if you start saving early. A 25-year-old will need to save about $7,405 annually, or $142 per week, to get there over 40 years, assuming an 8 percent annual return. Retirement account contributions from your employer will make it much easier to hit your retirement savings goal. If your employer matches your 401(k) contributions with $2,000 per year, you'll only need to save $104 per week to have $2 million by age 65, again assuming an 8 percent annual return.

Control costs. Minimizing investment fees and expenses will help you to grow your nest egg faster. That's because high expense ratios on mutual funds can have serious drag on your long-term returns. Getting a 7 percent annual return instead of 8 percent over a 40-year career (because you are paying 1 percent in yearly fees) means you will need to save $2,255 more per year to still hit $2 million by age 65. Index funds generally charge much less in annual fees than actively managed mutual funds. "If I didn't manage my own money, I would buy a S&P 500 index fund because it is low cost," says Farr.

Get a Roth IRA or 401(k). Roth 401(k)s and IRAs allow young people, who are likely to be in a low tax bracket, to pre-pay taxes on their retirement savings. "Young folks are in a lower tax bracket now than they will be in the future, including when they begin to tap into their retirement savings," says Joe Alfonso, a certified financial planner for Aegis Financial Advisory in Lake Oswego, Ore. "You're giving up the current tax deduction, but you are basically getting tax-free retirement income that would otherwise be taxable in the future." Once your contribution is made with after-tax dollars, that money can continue to grow for the rest of your life without the drag of taxes. If you wait until age 59½ to withdraw the money, you won't have to pay taxes on any of the growth.

Maximize Social Security. Social Security provides a base level of income that your retirement savings should build upon. Take steps to maximize the amount you get by making sure you have at least 35 years of earnings under your belt before you sign up for payments, so that zeros won't be factored into your calculation. And carefully consider the age at which you begin to claim benefits. Payouts increase for each year of delayed claiming between ages 62 and 70.

Don't plan on retiring at 65. A male born in 1946 can expect to live 18 years after retirement at age 66, according to Social Security Administration projections. Men born in 1980 should plan for at least a 19.3 year retirement, after the higher retirement age of 67. For women, the average projected length of retirement jumps from 20 years for those born in 1946 to 21.2 years for those born in 1980. And these are just the averages. "Generation Y's life expectancy is going to be a lot longer," says Farr. "They have to fund more years of retirement than the old financial planning models built in."

Of course, you don't have to retire at age 65, or at what the Social Security Administration defines as the full retirement age, which is 66 for most baby boomers and 67 for younger people. Working a few extra years gives you more time to save, allows your investments a longer time to compound, and reduces the number of retirement years your savings must finance. If you're 25 now and willing to work until age 70, you could reach $2 million by saving just $95 per week, assuming an 8 percent annual return and not even counting the 401(k) match.

Don't get hung up on the number. How much you need to save for retirement largely depends on your expenses. If you're willing to pay off your mortgage before retirement, move to a smaller house or low-cost area of the country, and live a modest lifestyle, you may find a way to get by on less. Conversely, those who want a lavish retirement will need to save more. "If you've got a goal based upon assumptions about inflation and rates of return, it's actually counterproductive, because those numbers can be pretty big, especially for young folks," says Alfonso. "It's more important to focus on the things that you can control, such as the percent of your gross income that you save and to really focus on your career and moving up the salary chain."

Monday, September 5, 2011

Formulating functional fitness for everyday people

NEW YORK (Reuters) -A mother-to-be hoists a rubber cylinder overhead. A 70-year-old balances on a wobble board and a firefighter grips a medicine ball while lunging across the gym floor.

Called functional training, workouts mirroring the activities of daily life have become a cornerstone of personal training sessions and group fitness classes, even if daily life can encompass anything from lifting a baby to scaling a burning building.

"Functional fitness has moved beyond the trend stage, and is simply one of the driving forces for many of the 50 million health club members," said Meredith Poppler of IHRSA (International Health, Racquet and Sportsclub Association).

It's basically exercise aimed at improving the quality of life and movement.

"Functional fitness is exercise that mimics everyday tasks," explained Frank Salzone, a trainer with the Equinox chain of fitness centers. "I always put my personal clients through functional training."

Salzone noted that while functional fitness has always been around, it has gained steam since the image of a healthy body shifted away from the bulkier body builder to today's leaner look.

"Body builders tend to use power moves, power lifting. They only do three or four repetitions at a time," he explained. "Functional training uses higher repetitions with fewer breaks so it boosts cardio vascular levels as well as strength training."

Bootcamp classes, which use light weights or one's own body weight, he said are among the most popular functional fitness classes.

"You can also use medicine balls, resistance balls, dumbbells," he said. "Any tool can be used in a group fitness setting given the right instruction and set up."

Among the newer tools in the functional fitness arsenal is the ViPR (Vitality, Performance, Reconditioning), a rubber cylinder with cutout handles designed to be carried, dragged, flipped, thrown, stepped on and rolled over.

It's functional, according to Salzone, because you can adjust your workout to your goals, "whether you're a marathoner, looking to gain lean mass or just have an overall full body workout."

Life Fitness, the Illinois-based equipment manufacturer, has put together functional training manuals specific to sports, such as football, basketball and baseball, as well as programs for seniors, youth and firefighters, according to spokesperson Heather Sieker.

"Functional training is basically a type of training that improves function," Sieker said. "It could be function in a specific sport, work, or even function in daily living."

Even absolute beginners can perform functional movements, she said, but they should ask the guidance of a fitness professional to start.

"Then as they progress they might incorporate more and more advanced movements," she said.

Salzone recommends starting out with three or four functional training sessions a week, then adding a day as you build strength.

"You should be doing four to five times a week for a full body functional workout," he said. "If you do these workouts nonstop, you'll be incorporating your cardio as well."

Salzone said you can define fitness in many ways.

"My definition of fit is having a healthy, well-working body where you're able to do functional movements without injuring yourself," he said. "If you're running for a bus, you want your heart rate to be able to go higher without risk."

Sunday, August 21, 2011

Scientists found cause of ALS (Lou Gehrig's disease)

(HealthDay News) -- The apparent discovery of a common cause of all forms of amyotrophic lateral sclerosis (ALS) could give a boost to efforts to find a treatment for the fatal neurodegenerative disease, a new study contends.

Scientists have long struggled to identify the underlying disease process of ALS (also known as Lou Gehrig's disease) and weren't even sure that a common disease process was associated with all forms of ALS.

In this new study, Northwestern University researchers said they found that the basis of ALS is a malfunctioning protein recycling system in the neurons of the brain and spinal cord. Efficient recycling of the protein building blocks in the neurons are critical for optimal functioning of the neurons. They become severely damaged when they can't repair or maintain themselves.

This problem occurs in all three types of ALS: hereditary, sporadic and ALS that targets the brain, the researchers said.

The discovery, published Aug. 21 in the journal Nature, shows that all forms of ALS share an underlying cause and offers a common target for drug therapy, according to the researchers.

"This opens up a whole new field for finding an effective treatment for ALS," study senior author Dr. Teepu Siddique, of the Davee Department of Neurology and Clinical Neurosciences at Northwestern's Feinberg School of Medicine, said in a university news release. "We can now test for drugs that would regulate this protein pathway or optimize it, so it functions as it should in a normal state."

This finding about the breakdown of protein recycling in ALS may also prove useful in the study of other neurodegenerative diseases, specifically Alzheimer's and other dementias, the Northwestern researchers said.

ALS afflicts an estimated 350,000 people around the world. About 50 percent of patients die within three years of the first symptoms. They progressively lose muscle strength until they're paralyzed and can't move, speak, swallow and breathe, the researchers said

Social Security disability on the brink of insolvency

WASHINGTON (AP) — Laid-off workers and aging baby boomers are flooding Social Security's disability program with benefit claims, pushing the financially strapped system toward the brink of insolvency.

Applications are up nearly 50 percent over a decade ago as people with disabilities lose their jobs and can't find new ones in an economy that has shed nearly 7 million jobs.

The stampede for benefits is adding to a growing backlog of applicants — many wait two years or more before their cases are resolved — and worsening the financial problems of a program that's been running in the red for years.

New congressional estimates say the trust fund that supports Social Security disability will run out of money by 2017, leaving the program unable to pay full benefits, unless Congress acts. About two decades later, Social Security's much larger retirement fund is projected to run dry as well.

Much of the focus in Washington has been on fixing Social Security's retirement system. Proposals range from raising the retirement age to means-testing benefits for wealthy retirees. But the disability system is in much worse shape and its problems defy easy solutions.

The trustees who oversee Social Security are urging Congress to shore up the disability system by reallocating money from the retirement program, just as lawmakers did in 1994. That would provide only short-term relief at the expense of weakening the retirement program.

Claims for disability benefits typically increase in a bad economy because many disabled people get laid off and can't find a new job. This year, about 3.3 million people are expected to apply for federal disability benefits. That's 700,000 more than in 2008 and 1 million more than a decade ago.

"It's primarily economic desperation," Social Security Commissioner Michael Astrue said in an interview. "People on the margins who get bad news in terms of a layoff and have no other place to go and they take a shot at disability,"

The disability program is also being hit by an aging population — disability rates rise as people get older — as well as a system that encourages people to apply for more generous disability benefits rather than waiting until they qualify for retirement.

Retirees can get full Social Security benefits at age 66, a threshold gradually rising to 67. Early retirees can get reduced benefits at 62. However, if you qualify for disability, you can get full benefits, based on your work history, even before 62.

Also, people who qualify for Social Security disability automatically get Medicare after two years, even if they are younger than 65, the age when other retirees qualify for the government-run health insurance program.

Congress tried to rein in the disability program in the late 1970s by making it tougher to qualify. The number of people receiving benefits declined for a few years, even during a recession in the early 1980s. Congress, however, reversed course and loosened the criteria, and the rolls were growing again by 1984.

The disability program "got into trouble first because of liberalization of eligibility standards in the 1980s," said Charles Blahous, one of the public trustees who oversee Social Security. "Then it got another shove into bigger trouble during the recent recession."

Today, about 13.6 million people receive disability benefits through Social Security or Supplemental Security Income. Social Security is for people with substantial work histories, and monthly disability payments average $927. Supplemental Security Income does not require a work history but it has strict limits on income and assets. Monthly SSI payments average $500.

As policymakers work to improve the disability system, they are faced with two major issues: Legitimate applicants often have to wait years to get benefits while many others get payments they don't deserve.

Last year, Social Security detected $1.4 billion in overpayments to disability beneficiaries, mostly to people who got jobs and no longer qualified, according to a recent report by the Government Accountability Office, the investigative arm of Congress.

Congress is targeting overpayments.

The deficit reduction package enacted this month would allow Congress to boost Social Security's budget by about $4 billion over the next decade to invest in programs that identify people who no longer qualify for disability benefits. The Congressional Budget Office estimates that increased enforcement would save nearly $12 billion over the next decade.

At the same time, the application process can be a nightmare for legitimate applicants. About two-thirds of initial applications are rejected. Most of these people drop their claims, but for those willing go through an appeals process that can take two years or more, chances are good they eventually will get benefits.

Astrue has pledged to reduce processing times for applicants' appeals, and he has had some success, even as the number of claims skyrockets. The number of people waiting for decisions has increased, but their wait times are going down.

"It's ludicrous to say that the backlog problem is getting worse," Astrue said. "The backlog problem has gotten dramatically better."

Patricia L. Foster said she was working as a nurse in a hospital in Columbia, S.C., in 2005 when she was attacked by a patient who was suffering from a mental illness. Foster, 64, said she injured her neck so bad she had a plate inserted. She said she also suffers from post-traumatic stress disorder.

Foster was turned down twice for Social Security disability benefits before finally getting them in 2009, after hiring an Illinois-based company, Allsup, to represent her. She said she was awarded retroactive benefits, though the process was demeaning.

"I have to tell you, when you're told you cannot return to nursing because of your disability, you don't know how long I cried about that," Foster said. "And then Social Security says, 'Oh no, you don't qualify.' You don't know what that does to you emotionally. You have no idea."

Sunday, April 3, 2011

Health Insurance Ruling Appealed

The health insurance overhaul program ruling that it was unconstitutional is being appealed by the Justice Department.

President Barack Obama’s administration passed the healthcare reform a year ago and the Justice Department has now appealed a judge’s ruling that struck down the federal overhaul.

The Justice Department said the federal health care overhaul's core requirement to make virtually all citizens buy health insurance or face tax penalties is constitutional because Congress has the authority to regulate interstate business.

The government's 62-page motion filed Friday to the 11th Circuit Court of Appeals argued that Congress has the power granted in the overhaul due to "rational means of regulating the way participants in the health care market pay for their services."

President Barack Obama’s administration passed the healthcare reform a year ago and the Justice Department has now appealed a judge’s ruling that struck down the federal overhaul.

The Justice Department said the federal health care overhaul's core requirement to make virtually all citizens buy health insurance or face tax penalties is constitutional because Congress has the authority to regulate interstate business.

The government's 62-page motion filed Friday to the 11th Circuit Court of Appeals argued that Congress has the power granted in the overhaul due to "rational means of regulating the way participants in the health care market pay for their services."

The appeal also warns that other segments of the program, including a law that blocks insurers from denying coverage to people because of pre-existing conditions, would be "unworkable" without a minimum coverage provision.

Subscribe to:

Posts (Atom)